INSIGHTS FROM THE PRIVATE BANK

2026 Outlook

Brett Mitstifer, CFA

Flagstar Chief Investment Officer

INSIGHTS FROM THE PRIVATE BANK

Brett Mitstifer, CFA

Flagstar Chief Investment Officer

The idea of fiscal and monetary policy working in harmony to propel economic growth is both compelling and complex. In theory, synchronized stimulus can create a powerful tailwind for the economy—lower borrowing costs from monetary easing combined with targeted government spending can amplify demand, investment, and confidence. However, this alignment is more aspirational than assured.

Synergy between these two levers faces structural challenges. Inflation remains the primary risk: re-acceleration driven by economic shocks or wage pressures could force the Fed to pause, breaking the narrative of coordination. Meanwhile, escalating federal debt and interest payments limit fiscal flexibility. Political fragmentation compounds uncertainty, as legislative consensus is essential to fiscal action. Global risks—from geopolitical tensions to commodity volatility—further complicate sustained alignment.

Despite these headwinds, 2026 offers a window where alignment is achievable. If inflation remains contained and productivity-led growth continues, both levers could support stimulus—lower rates paired with targeted fiscal spending. Structural investments in infrastructure, AI, and industrial technology can complement monetary easing, fostering productivity gains without immediate inflationary spikes.

“Two Levers, One Lift” is a strategic narrative for optimism, not a guaranteed outcome. Alignment is conditional, not permanent. Investors should position for potential synergy but remain vigilant to risks—particularly inflation, debt dynamics, and political constraints—that could force rapid divergence.

In 2026, the U.S. economy can secure a soft landing and re accelerate if policymakers align both levers: monetary easing as inflation and tariff pass through fade, and fiscal stimulus via the OBBBA and pragmatic regulatory reforms. Together, these actions reinforce demand, lower financing frictions, and unlock productivity investment—the essence of “Two Levers, One Lift.”

Following 2025’s pivot from peak restrictive settings, major investment houses and economic forecasters expect two quarter point cuts in 2026—often penciled in for March and mid year—bringing the funds rate toward 3.0–3.25%, provided inflation’s glidepath continues and labor markets soften. Forecasts explicitly factor in tariff related price pressures peaking in early 2026 and receding by mid year, lowering the need for restrictive policy while preserving vigilance on price stability.

While the precise pace of cuts remains debated, committee dispersion coexists with broad market bias toward supporting growth as core inflation trends ease and the labor markets cool.

The OBBBA—signed into law July 4, 2025—delivers a multi channel boost to households and businesses: no tax on tips, no tax on overtime, expanded deductions (including SALT mechanics), and income tax adjustments that raise disposable income and near term consumption.

On the corporate side, making 100% bonus depreciation and R&D expensing permanent improves after tax returns on capital, accelerating equipment, software, and factory investment—especially in manufacturing and energy adjacent industries.

Independent modeling suggests the bill provides a moderate growth impulse into 2026—roughly ~0.5 percentage points to GDP—tempered by interactions with tariffs and spending offsets; its impact amplifies when paired with deregulatory steps that lower compliance costs and speed project deployment.

Sources: IRS, Kiplinger, Tax Foundation, Oxford Economics, JPMorgan Asset Management

Artificial intelligence is emerging as a structural productivity driver, enabling businesses to produce more output with fewer inputs—whether through automation, predictive analytics, or streamlined decision making. A productivity driven economy can grow without igniting inflation because efficiency gains expand supply capacity, offsetting demand side pressures. When firms can scale output without proportionate increases in labor or capital costs, unit costs fall, margins improve, and price stability holds even as GDP accelerates. AI driven productivity creates a virtuous cycle: higher growth potential, stronger competitiveness, and muted inflation risk—allowing policymakers to support expansion without fearing an overheating economy.

If the Fed trims rates toward 3–3.25% while OBBBA’s tax cuts and regulatory reforms continue to filter through, positioning should favor:

Source: Goldman Sachs, Moneycontrol, Investopedia, AInvest, Oxford Economics

The global equity market enters 2026 with strong momentum, anchored by a continuation of the U.S. bull market. Historical trends suggest that three consecutive years of positive returns often lead to a fourth, and fundamentals support this view. U.S. earnings growth projects at 15% for the S&P 500, far exceeding the 5–10% expected in the Eurozone. This earnings strength, combined with favorable macro conditions, positions U.S. equities as the primary driver of global performance.

Source: Barrons

Monetary policy and fiscal measures will provide additional tailwinds. The Federal Reserve’s anticipated rate cuts should ease financial conditions, while corporate tax relief through accelerated depreciation under OBBB adds to profitability. Rising productivity from AI adoption further enhances margins and efficiency, creating a compelling backdrop for U.S. companies. AI-driven automation and advanced analytics are accelerating operational efficiencies, reducing costs, and enabling firms to scale without proportional increases in labor. These trends are particularly impactful in sectors such as manufacturing, logistics, and financial services, where AI is improving decision-making and unlocking new revenue streams.

However, investors should remain mindful of risks and volatility. While tariff-related pressures are expected to ease, geopolitical uncertainty, potential policy missteps, and lingering inflationary forces could introduce bouts of market turbulence. Europe faces structural impediments and slower growth, while China’s economy remains constrained by weak consumer spending and challenges in real estate and banking. These factors could amplify volatility in global markets, particularly if currency fluctuations or unexpected rate adjustments occur.

In this environment, global diversification remains prudent, with emphasis on U.S. equities—including small caps—and selective exposure to Japan, which benefits from stimulative policies and regulatory reforms. While the outlook is constructive, investors should prepare for a higher-volatility regime compared to prior years, using risk management strategies such as sector rotation, quality bias, and tactical hedging to navigate potential shocks. Companies leveraging AI effectively may offer a defensive edge, as productivity gains and innovation-driven growth can help offset margin pressures during periods of uncertainty.

Market history offers strong precedent for the themes shaping 2026. Multi-year bull markets often persist: over 150 years of U.S. equity data show that 69% of years deliver positive returns, and extended uptrends frequently follow periods of strong earnings and accommodative policy. Similarly, past Federal Reserve easing cycles have coincided with robust equity performance—studies indicate that during rate-cut periods, the S&P 500 rose 67% of the time, with cumulative gains averaging roughly 30%, even amid heightened volatility.

On the productivity front, AI adoption mirrors transformative trends seen during the IT boom of the 1990s. Research suggests AI-driven efficiency gains could add 0.1% to 2.0% annually to productivity growth, reinforcing margin expansion and competitive advantages for firms embracing automation and advanced analytics. These historical patterns underscore why the combination of strong earnings, policy support, and technological innovation creates a compelling backdrop for equities—while reminding investors that volatility often accompanies such inflection points.

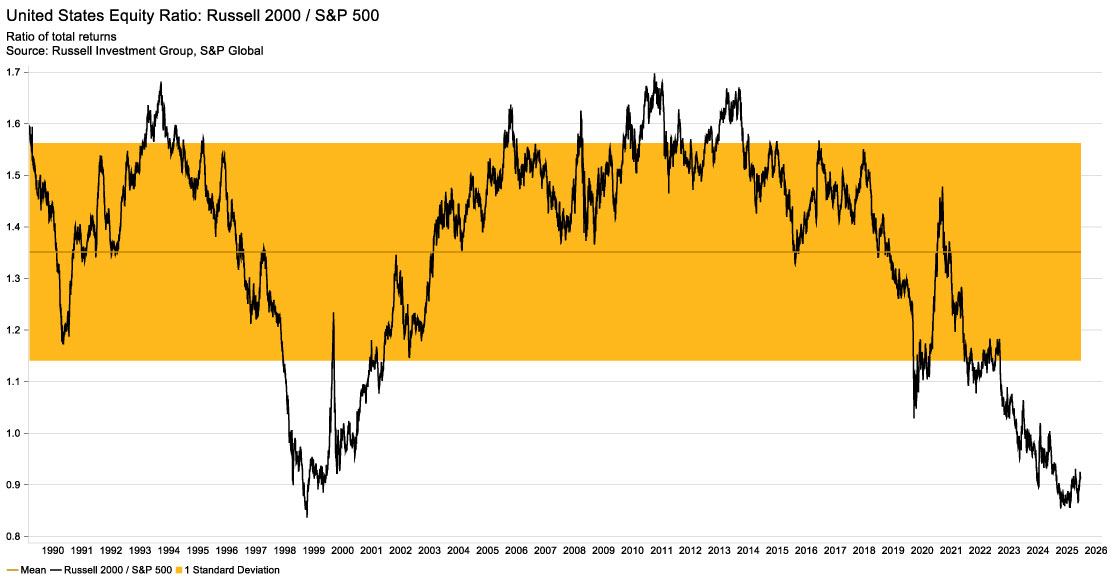

While the “Magnificent Seven” have dominated equity returns in recent years, 2026 presents an opportunity for market leadership to broaden beyond mega-cap technology. Economic growth, rising productivity, and lower interest rates create a favorable backdrop for small-cap stocks, which tend to outperform during periods of accelerating activity and easing financial conditions. As borrowing costs decline and AI-driven efficiencies spread across industries, smaller companies stand to benefit disproportionately from improved margins and expanding demand. This broadening of market participation not only enhances diversification but also signals a healthier, more sustainable bull market, reducing concentration risk and opening new avenues for alpha generation.

Source: Russell, S&P, CFA Institute

Source: Russell, S&P, CFA Institute

The Federal Reserve enters 2026 with a clear easing bias. Following a series of cuts in late 2025, additional rate reductions are anticipated as inflation normalizes and labor markets stabilize. Importantly, these moves aren’t reactive to recessionary conditions—growth remains positive, supported by consumer resilience and ongoing fiscal initiatives in infrastructure and industrial policy. This rare alignment of monetary and fiscal levers creates a constructive backdrop for fixed income investors.

The yield curve is expected to steepen modestly as short-term rates decline more aggressively than long-term yields. However, the overall curve should shift downward, reflecting lower policy rates and anchored inflation expectations. This environment favors duration strategies, particularly in intermediate maturities, where investors can capture yield before the curve fully adjusts. While volatility may persist due to global macro uncertainties, the directional bias toward lower yields provides a tailwind for total return strategies.

Corporate credit spreads remain historically tight, underscoring strong fundamentals and investor confidence. Yet, this tightness limits broad-based upside, making selectivity paramount. Investors should prioritize issuers with robust balance sheets, resilient cash flows, and disciplined capital allocation. Sectors tied to secular growth themes—such as technology infrastructure and renewable energy—offer relative value, while over-leveraged or cyclical names warrant caution. Active management will be critical to avoid asymmetric risk in a low-spread environment.

Municipal bonds continue to stand out as an attractive option for tax-sensitive investors. Solid credit quality across most issuers, combined with favorable technicals and competitive tax-equivalent yields, reinforces their appeal. State and local revenues remain stable, supported by economic growth and prudent fiscal management. Longer-dated municipal bonds offer compelling opportunities for those seeking to lock in after-tax income in a declining rate environment.

2026 offers favorable conditions for fixed income investors: additional Fed easing, no recession, and a yield curve trending lower create opportunities across duration and high-quality spread sectors. With corporate spreads tight, selectivity is key, while municipal bonds remain a cornerstone for stability and tax efficiency.

Agentic AI is poised to redefine enterprise workflows in 2026, moving beyond automation into autonomous decision-making and task execution. Adoption is accelerating across sectors as firms seek to unlock productivity gains, streamline operations, and enhance customer engagement. This shift represents a structural transformation in how businesses allocate human capital and leverage data. Companies integrating agentic AI effectively will likely achieve margin expansion and competitive differentiation, making this theme a cornerstone of digital innovation strategies.

Gold and silver continue to shine as strategic portfolio diversifiers in 2026, supported by persistent geopolitical tensions, robust central bank buying, and a structurally weaker U.S. dollar. These dynamics reinforce the appeal of precious metals as hedges against uncertainty and currency depreciation. While volatility may persist, the underlying momentum remains intact, offering investors a compelling way to balance risk and preserve purchasing power in an environment where traditional safe havens face valuation pressures.

Homebuilders and housing-related equities, long out of favor as NAHB sentiment hovered below 50, are positioned for a contrarian rebound in 2026. The catalyst: a sustained decline in interest rates and additional Fed cuts, which improve affordability and stimulate demand. While supply constraints and regulatory hurdles remain, the combination of easing financial conditions and pent-up household formation suggests a recovery trajectory. Investors willing to lean into this theme may capture upside as housing transitions from laggard to leader.

After years of concentration risk, 2026 is shaping up as a year of market broadening, with improved relative performance from the S&P 493 and small-cap stocks. This shift reflects a healthier market structure, driven by easing monetary policy, stabilizing economic growth, and valuation normalization outside mega-cap tech. Broader participation enhances diversification benefits and signals a more sustainable equity rally. For investors, tilting toward underrepresented segments could unlock alpha as leadership rotates beyond the narrow confines of prior years.

1. Embrace volatility – Market swings create opportunity

2. Stay invested – Time in the market beats timing the market

3. Diversify broadly – Across asset classes, sectors, and geographies

4. Manage risk first – Define downside before committing capital

5. Maintain liquidity – Avoid forced selling in stress periods

6. Think long-term – Compounding drives wealth creation

7. Control behavior – Recognize fear and greed; stay disciplined

8. Adapt strategically – Markets evolve, so should your approach

9. Optimize taxes – Tax efficiency enhances net returns

10. Plan for uncertainty – Hedge geopolitical and currency risks

Please reach out with any questions or to discuss portfolio positioning in more detail. We appreciate your continued trust and partnership.

If you are an existing customer and have Account related questions, please contact Customer Support.

Thank you for your feedback

Form submitted succesfully

By clicking submit, you understand the information is being provided to Flagstar Bank in accordance with our online privacy statement.

Important Legal Disclosures and Information

These materials are intended for distribution to Flagstar Private Bank clients, and do not constitute the provision of investment, legal, accounting, or tax advice to any person. This material presented is for informational purposes only and is not intended to be an offer, recommendation, or solicitation to purchase or sell any security or product, or to employ a specific investment or tax planning strategy. Forward looking projections are based on historical trends, actual results will differ. Past performance is no guarantee of future results.

The information contained herein was obtained from sources deemed reliable. Such information is not guaranteed as to its accuracy, timeliness, or completeness. The information contained and the opinions expressed herein are subject to change without notice, are those of the individual author(s), and may not necessarily represent the views of Flagstar Bank or any of its subsidiaries.

Flagstar Private Bank is a division of Flagstar Bank, N.A. (“Flagstar Bank”), Member FDIC. Flagstar Bank provides FDIC-insured banking products and services and lending of funds to individual clients. Securities, insurance, brokerage services, and investment advisory services are offered by Flagstar Securities, Inc. (“Flagstar Securities”), Member FINRA/SIPC, a registered broker-dealer and SEC registered investment adviser. Flagstar Securities is a wholly-owned subsidiary of Flagstar Bank.

Investments, Brokerage and Insurance Products Are:

Not Insured by the FDIC or Any Other Government Agency. | Not Bank Guaranteed. | Not Bank Deposits or Obligations. | May Lose Value.

|

Flagstar Securities Client Relationship Summary

Flagstar Securities Regulatory Summaries and Disclosures