INSIGHTS FROM THE PRIVATE BANK

After the Shock: Pulling on the Same Levers

Brett Mitstifer, CFA

Flagstar Chief Investment Officer

FDIC-Insured—Backed by the full faith and credit of the U.S. Government

INSIGHTS FROM THE PRIVATE BANK

Brett Mitstifer, CFA

Flagstar Chief Investment Officer

Geopolitical shocks increased volatility, not fragility. The Iran war introduced nearterm uncertainty, but core economic and market fundamentals remained intact.

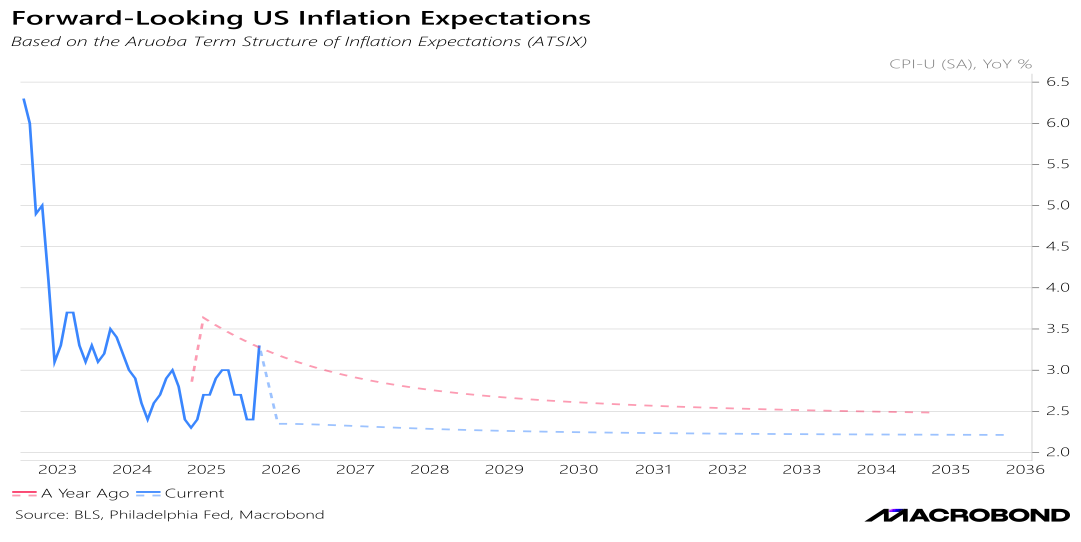

Monetary policy optionality remains alive. While the Iran conflict complicated the Fed’s nearterm calculus, longerterm inflation expectations (3 and 5 year) remain well anchored, preserving the path for rate cuts.

Leadership change matters. The installation of a new Fed Chair in June creates a credible inflection point for recalibrating policy and reintroducing rate cuts in the second half of 2026.

Fiscal policy and AI investment continue to lift growth. Supportive fiscal measures and sustained AI driven CAPEX underpin productivity gains and economic resilience.

Markets are confirming the macro narrative. Rising earnings expectations, broadening equity leadership, and the normalization of credit spreads all signal continued confidence in the U.S. expansion.

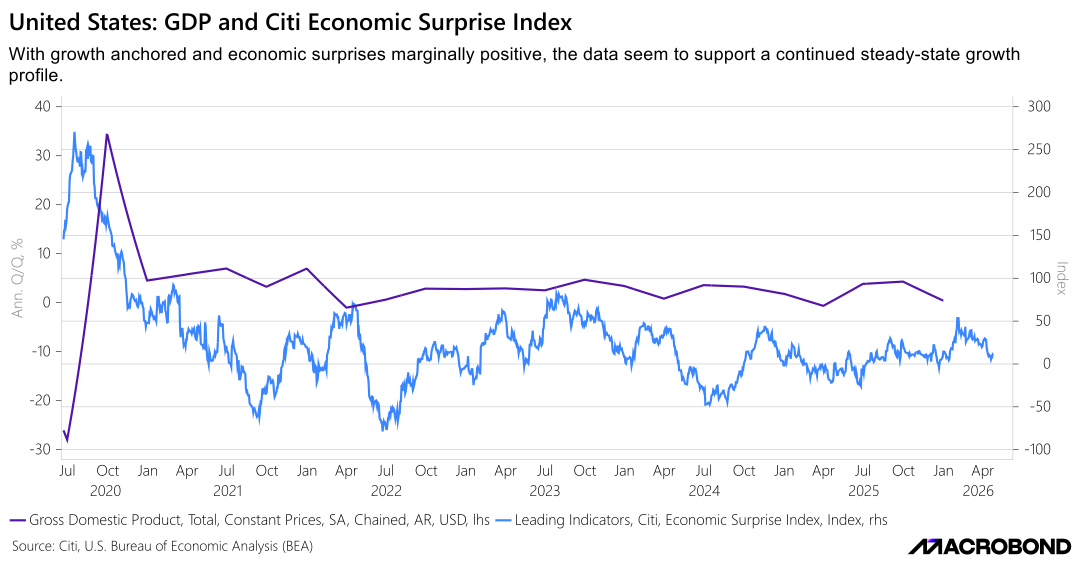

The first quarter of 2026 represented a transition phase for both markets and the broader economy—marked by heightened volatility, rising geopolitical tension, and clear signs of underlying resilience. Economic growth moderated from prior rates but remained solid, even as restrictive monetary policy and global uncertainty weighed on sentiment. These pressures intensified as military conflict involving Iran erupted during the quarter, disrupting energy markets and triggering a risk‑off episode in March.

Equity markets responded swiftly but orderly to these shocks. The selloff was concentrated in mega‑cap growth and rate‑sensitive segments, while broader market participation held firm. First‑quarter index returns reflect this internal divergence: the S&P 500 declined ‑4.6%, the Dow Jones Industrial Average fell ‑3.6%, and the Nasdaq retreated ‑7.1%. In contrast, the Russell 2000 rose +0.6% and the S&P 500 Equal Weight Index gained +0.2%, underscoring improving breadth beneath headline weakness.

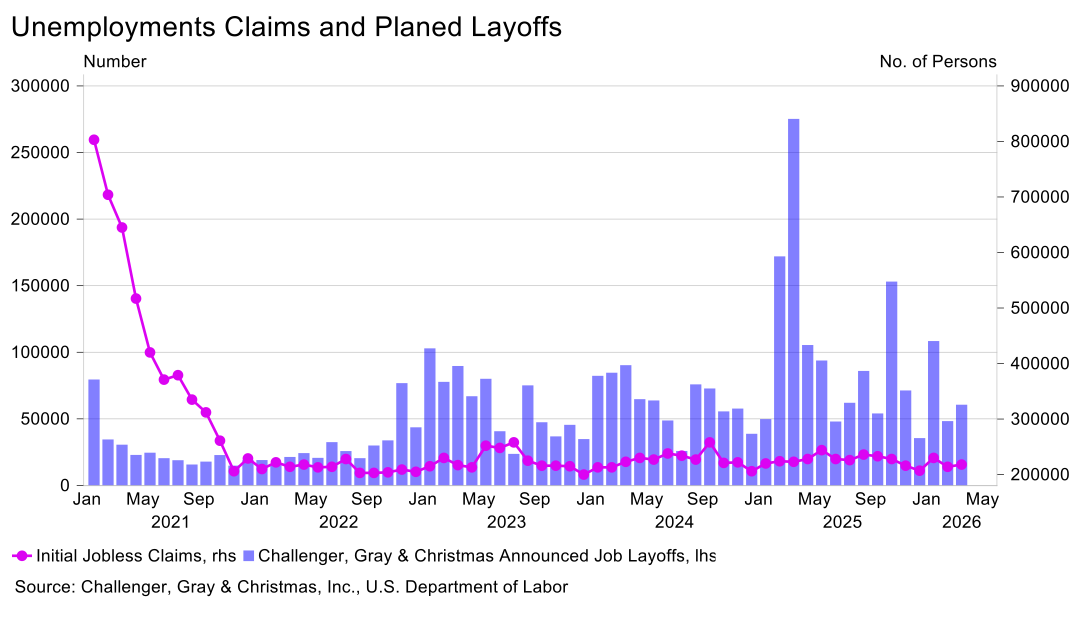

Economic data throughout the quarter reinforced this message of resilience. Labor markets remained stable across multiple measures. Non‑farm payroll growth continued at a pace consistent with trend expansion, weekly initial jobless claims remained historically low and well contained, and ADP private employment reports confirmed ongoing hiring momentum. Collectively, these indicators point to a labor market cooling gradually—but not deteriorating.

The U.S. consumer also remained a durable source of support. Retail sales surprised to the upside, reflecting steady employment, wage income, and fiscal tailwinds. Housing, however, remained a notable area of weakness, as elevated mortgage rates continued to pressure affordability, home sales, and transaction volumes. Taken together, first quarter data pointed to an economy rebalancing under tighter financial conditions rather than sliding into contraction.

Looking through the balance of 2026, the U.S. economy remains supported by the potential alignment of fiscal and monetary policy—the same “Two Levers, One Lift” framework that has underpinned the post‑pandemic expansion. Fiscal policy remains firmly intact and supportive. Existing legislation, deregulation, and targeted incentives continue to reinforce household consumption, business confidence, and private‑sector investment.

A defining structural theme remains the acceleration of capital expenditures tied to artificial intelligence. Investment in data centers, automation, semiconductor manufacturing, and related infrastructure continues at a strong pace. These investments are not merely cyclical; they are driving productivity improvements that expand supply side capacity, allowing the economy to grow without reigniting sustained inflation. Importantly, productivity gains also help offset labor uncertainty associated with adoption of AI, easing one of the Fed’s key policy constraints.

The Iran war has added complexity to the near term outlook, particularly for monetary policymakers. Oil price volatility complicates headline inflation readings and temporarily raises the bar for near term easing. Crucially, however, longer term inflation expectations—measured across three and five year horizons—have remained well anchored. This stability reinforces confidence that inflation pressures tied to energy represent a cyclical shock rather than a structural regime shift.

The Federal Open Market Committee faces a more challenging tradeoff than earlier in the cycle. Elevated headline inflation driven by energy contrasts with stable core inflation trends, placing policymakers in a position where patience is required but flexibility remains intact. While the Iran conflict delayed near term rate cuts, monetary policy is no longer tightening.

A key inflection point arrives in June with the installation of a new Federal Reserve Chair. This leadership transition creates an opportunity for recalibration as policymakers assess improving productivity, stable core inflation, and a labor market that remains resilient despite AI related uncertainty. As energy related pressures normalize, the door for rate cuts in the second half of 2026 could reopen quickly, particularly in an environment where productivity gains help contain inflation even as growth remains firm.

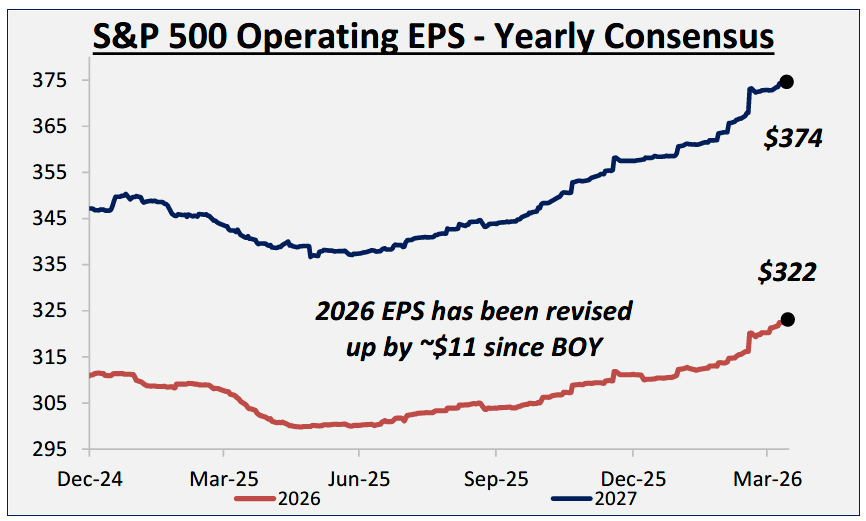

Equity markets continue to find strong support in fundamentals rather than liquidity alone. Notably, earnings estimates rose during the Iran conflict—an unusual and powerful signal of corporate resilience. Consensus forecasts now call for approximately 18% earnings growth in 2026, reflecting durable margins, stable demand, and ongoing productivity gains.

Market leadership has also broadened meaningfully. Small cap equities are now leading large caps, a historical pattern typically associated with periods of strong economic growth and easing financial conditions. Smaller companies tend to benefit disproportionately from declining borrowing costs and improving domestic activity, reinforcing the signal that underlying growth momentum remains intact.

Equity market strength continues to support the household wealth effect, bolstering consumer confidence and spending. When combined with stable employment and supportive fiscal policy, this dynamic contributes to a continued low probability of recession despite episodic volatility.

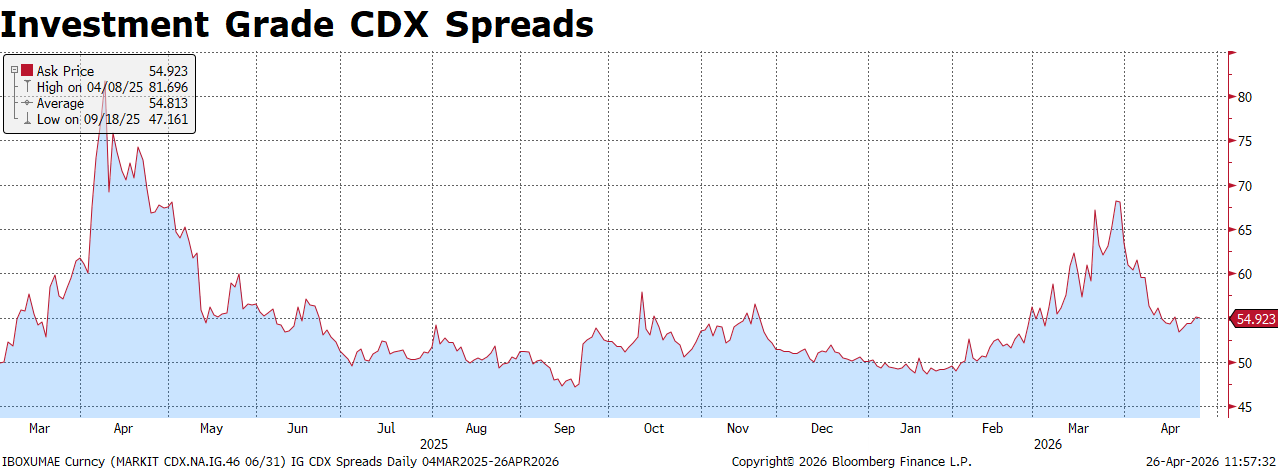

Fixed income markets have provided an important real time assessment of economic resilience. During the height of the Iran conflict, investment grade credit spreads widened modestly as investors priced in energy driven inflation risks and a more cautious Federal Reserve. Importantly, this widening was orderly and contained-characteristics of uncertainty rather than systemic stress.

As signs emerged that the conflict was winding down and a ceasefire took hold, those same investment‑grade spreads retraced their move and now sit near pre‑war levels. This normalization represents a clear vote of confidence from credit markets in the durability of the U.S. economy, the strength of corporate balance sheets, and the sustainability of cash flows.

While oil‑related inflation complicated the timing of rate cuts, longer‑term inflation expectations remain anchored, and credit markets continue to indicate a low probability of recession. High‑quality fixed income remains a core portfolio anchor, offering income, diversification, and optionality as monetary policy ultimately shifts toward accommodation.

The post shock environment of 2026 continues to favor disciplined risk taking. Supportive fiscal policy, accelerating productivity from AI investment, resilient earnings growth, and stabilizing credit conditions together form a constructive backdrop for risk assets.

Geopolitical risks and policy uncertainty are unlikely to disappear, but they have not undermined the structural foundations of expansion. With both policy levers still capable of pulling in the same direction after the shock, investors should remain positioned for growth—embracing volatility as opportunity rather than risk.

Agentic AI is poised to redefine enterprise workflows in 2026, moving beyond automation into autonomous decision-making and task execution. Adoption is accelerating across sectors as firms seek to unlock productivity gains, streamline operations, and enhance customer engagement. This shift is not just incremental—it represents a structural transformation in how businesses allocate human capital and leverage data. Companies that integrate agentic AI effectively will likely see margin expansion and competitive differentiation, making this theme a cornerstone of digital innovation strategies.

Gold and silver continue to shine as strategic portfolio diversifiers in 2026, supported by persistent geopolitical tensions, robust central bank buying, and a structurally weaker U.S. dollar. These dynamics reinforce the appeal of precious metals as a hedge against uncertainty and currency depreciation. While volatility may persist, the underlying momentum remains intact, offering investors a compelling way to balance risk and preserve purchasing power in an environment where traditional safe havens face valuation pressures.

Homebuilders and housing-related equities, long out of favor as NAHB sentiment hovered below 50, are positioned for a contrarian rebound in 2026. The catalyst: a sustained decline in interest rates and additional Fed cuts, which improve affordability and stimulate demand. While supply constraints and regulatory hurdles remain, the combination of easing financial conditions and pent-up household formation suggests a recovery trajectory. Investors willing to lean into this theme may capture upside as housing transitions from laggard to leader.

After years of concentration risk, 2026 is shaping up as a year of market broadening, with improved relative performance from the S&P 493 and small-cap stocks. This shift reflects a healthier market structure, driven by easing monetary policy, stabilizing economic growth, and valuation normalization outside mega-cap tech. Broader participation enhances diversification benefits and signals a more sustainable equity rally. For investors, tilting toward underrepresented segments could unlock alpha as leadership rotates beyond the narrow confines of prior years.

Please reach out with any questions or to discuss portfolio positioning in more detail. We appreciate your continued trust and partnership.

If you are an existing customer and have Account related questions, please contact Customer Support.

Thank you for your feedback

Form submitted succesfully

By clicking submit, you understand the information is being provided to Flagstar Bank in accordance with our online privacy statement.

Important Legal Disclosures and Information

These materials are intended for distribution to Flagstar Private Bank clients, and do not constitute the provision of investment, legal, accounting, or tax advice to any person. This material presented is for informational purposes only and is not intended to be an offer, recommendation, or solicitation to purchase or sell any security or product, or to employ a specific investment or tax planning strategy. Forward looking projections are based on historical trends, actual results will differ. Past performance is no guarantee of future results.

The information contained herein was obtained from sources deemed reliable. Such information is not guaranteed as to its accuracy, timeliness, or completeness. The information contained and the opinions expressed herein are subject to change without notice, are those of the individual author(s), and may not necessarily represent the views of Flagstar Bank or any of its subsidiaries.

Flagstar Private Bank is a division of Flagstar Bank, N.A. (“Flagstar Bank”), Member FDIC. Flagstar Bank provides FDIC-insured banking products and services and lending of funds to individual clients. Securities, insurance, brokerage services, and investment advisory services are offered by Flagstar Securities, Inc. (“Flagstar Securities”), Member FINRA/SIPC, a registered broker-dealer and SEC registered investment adviser. Flagstar Securities is a wholly-owned subsidiary of Flagstar Bank.

Investments, Brokerage and Insurance Products Are:

Not Insured by the FDIC or Any Other Government Agency. | Not Bank Guaranteed. | Not Bank Deposits or Obligations. | May Lose Value.

|

Flagstar Securities Client Relationship Summary

Flagstar Securities Regulatory Summaries and Disclosures