INSIGHTS FROM THE PRIVATE BANK

Like Oil and Water (pun intended)

Brett Mitstifer, CFA

Flagstar Chief Investment Officer

FDIC-Insured—Backed by the full faith and credit of the U.S. Government

INSIGHTS FROM THE PRIVATE BANK

Brett Mitstifer, CFA

Flagstar Chief Investment Officer

Markets have an interesting way of absorbing shocks—sometimes with drama, other times with a calm that feels almost counterintuitive. The unfolding conflict involving Iran has injected a new level of geopolitical risk into the narrative, yet the market response so far has been surprisingly orderly. Much like oil and water, the forces shaping today’s investment environment appear fundamentally different in nature, yet they are coexisting in the same container. The resulting dichotomy is defining the current landscape.

At the macro level, significant geopolitical tensions would normally be expected to trigger sharp risk-off behavior. Energy markets, unsurprisingly, have been the most sensitive barometer. Oil prices have reacted to the prospect of supply disruption and elevated shipping risk through the most critical of corridors, while defense-related equities have also seen increased attention. Yet the broader equity market response has been measured rather than panicked. Major indices have largely maintained their footing, reflecting a market that has become adept at compartmentalizing geopolitical events from the underlying economic trajectory.

This composure highlights the first major divide in markets today: headline risk versus economic momentum. Corporate earnings remain resilient, consumer spending has moderated but not collapsed, and capital investment, particularly in technology, continues to surprise to the upside. Investors appear willing to treat geopolitical flare-ups as episodic rather than structural disruptions to global growth.

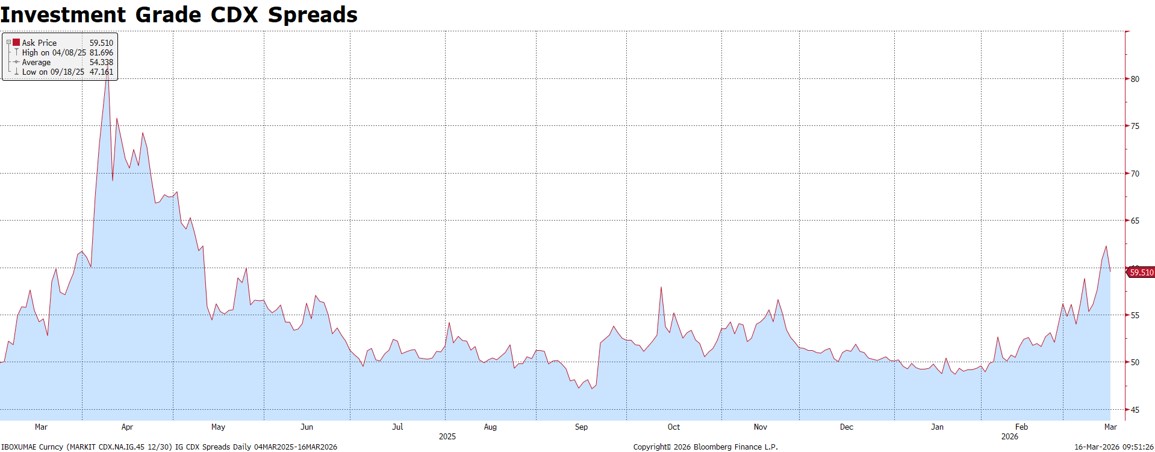

Credit markets reveal another fascinating divergence. Investment-grade spreads remain relatively contained, reflecting strong corporate balance sheets, ample liquidity, and continued demand from institutional investors. In contrast, private credit markets are showing signs of stress at the margin. Higher base rates and tighter refinancing conditions are beginning to pressure highly levered borrowers in certain sectors. This isn’t yet systemic stress, but it does underscore a growing separation between public market transparency and the more opaque dynamics within private lending structures. In essence, the public markets are calm while some private corners of credit are quietly recalibrating.

A similar “oil and water” dynamic is playing out in the labor market narrative. On one hand, the rapid evolution of artificial intelligence raises legitimate questions about the long-term structure of employment. Entire job categories—from routine administrative work to certain forms of knowledge processing—may face meaningful disruption over time. Yet policymakers, particularly the Federal Reserve, remain firmly focused on the challenge of inflation. Wage growth, services inflation, and the durability of consumer demand continue to dominate the policy conversation. The contrast is striking; markets are debating the future of work while central bankers remain focused on the current price cycle.

This juxtaposition—technological disruption versus cyclical inflation management—illustrates how multiple economic timelines are unfolding simultaneously. Investors are navigating both the structural transformation of the global economy and the traditional rhythms of monetary policy.

Despite the complexity, markets have demonstrated an encouraging level of resilience. Volatility has increased around the edges, particularly in commodities, rates, and certain credit segments, but the core of the financial system remains stable. Corporate balance sheets are healthier than in previous cycles, banks are well-capitalized, and global liquidity, while no longer excessively abundant, remains supportive.

For long-term investors, this environment may feel uncomfortable—but it is also familiar. Periods where narratives collide often create the most compelling entry points. When geopolitical risk intersects with technological transformation and monetary recalibration, price discovery becomes more dynamic. And that is precisely where opportunity emerges.

Markets, like oil and water, may appear to be moving in opposing directions today. But over time, these competing forces tend to settle into an equilibrium. As geopolitical headlines evolve, inflation continues its gradual long-term descent, and productivity gains from technology begin to materialize, the underlying trajectory for risk assets remains constructive.

History reminds us that uncertainty rarely lasts forever—but the opportunities it creates often do. Volatility creates opportunity, and the current environment suggests that those opportunities are likely to unfold positively in the months ahead.

Please reach out with any questions or to discuss portfolio positioning in more detail. We appreciate your continued trust and partnership.

If you are an existing customer and have Account related questions, please contact Customer Support.

Thank you for your feedback

Form submitted succesfully

By clicking submit, you understand the information is being provided to Flagstar Bank in accordance with our online privacy statement.

Important Legal Disclosures and Information

These materials are intended for distribution to Flagstar Private Bank clients, and do not constitute the provision of investment, legal, accounting, or tax advice to any person. This material presented is for informational purposes only and is not intended to be an offer, recommendation, or solicitation to purchase or sell any security or product, or to employ a specific investment or tax planning strategy. Forward looking projections are based on historical trends, actual results will differ. Past performance is no guarantee of future results.

The information contained herein was obtained from sources deemed reliable. Such information is not guaranteed as to its accuracy, timeliness, or completeness. The information contained and the opinions expressed herein are subject to change without notice, are those of the individual author(s), and may not necessarily represent the views of Flagstar Bank or any of its subsidiaries.

Flagstar Private Bank is a division of Flagstar Bank, N.A. (“Flagstar Bank”), Member FDIC. Flagstar Bank provides FDIC-insured banking products and services and lending of funds to individual clients. Securities, insurance, brokerage services, and investment advisory services are offered by Flagstar Securities, Inc. (“Flagstar Securities”), Member FINRA/SIPC, a registered broker-dealer and SEC registered investment adviser. Flagstar Securities is a wholly-owned subsidiary of Flagstar Bank.

Investments, Brokerage and Insurance Products Are:

Not Insured by the FDIC or Any Other Government Agency. | Not Bank Guaranteed. | Not Bank Deposits or Obligations. | May Lose Value.

|

Flagstar Securities Client Relationship Summary

Flagstar Securities Regulatory Summaries and Disclosures