INSIGHTS FROM THE PRIVATE BANK

The Power of Equanimity: Navigating Volatile Markets with Composure

Brett Mitstifer, CFA

Flagstar Chief Investment Officer

INSIGHTS FROM THE PRIVATE BANK

Brett Mitstifer, CFA

Flagstar Chief Investment Officer

“Equanimity” - evenness of mind especially under stress, a state in which you remain balanced and not easily thrown by shocks, disappointment or pressure.

The second quarter of 2026 marked a decisive transition from geopolitical shock to market relief, and it underscored the value of equanimity — defined here as an evenness of mind under stress, disappointment, or pressure. The quarter began with investors still processing the economic and inflationary fallout from the Iran War, the blockade of the Strait of Hormuz, and the risk that energy prices could force the Federal Reserve into a more restrictive stance. As military activity gave way to a fragile ceasefire and then to a signed U.S.–Iran MOU providing 60 days for negotiation, markets began to discount a lower probability of open-ended disruption.

The relief rally was substantial. Equity markets recovered as the probability of a more durable reopening of energy flows improved, oil prices retreated, and the geopolitical risk premium compressed. Importantly, crude finished the quarter only marginally above prewar levels, reducing the risk that headline inflation would remain contaminated by the energy shock for an extended period.

The policy narrative also changed materially. At mid-quarter, expectations for rate cuts gave way to concern that the new Fed Chair, Chairman Warsh, might inherit an inflation problem severe enough to require renewed tightening. By quarter-end, however, lower oil prices, contained credit stress, and a still-stable labor market shifted the base case back toward a pause: no cuts in the immediate term, but no rate hikes either.

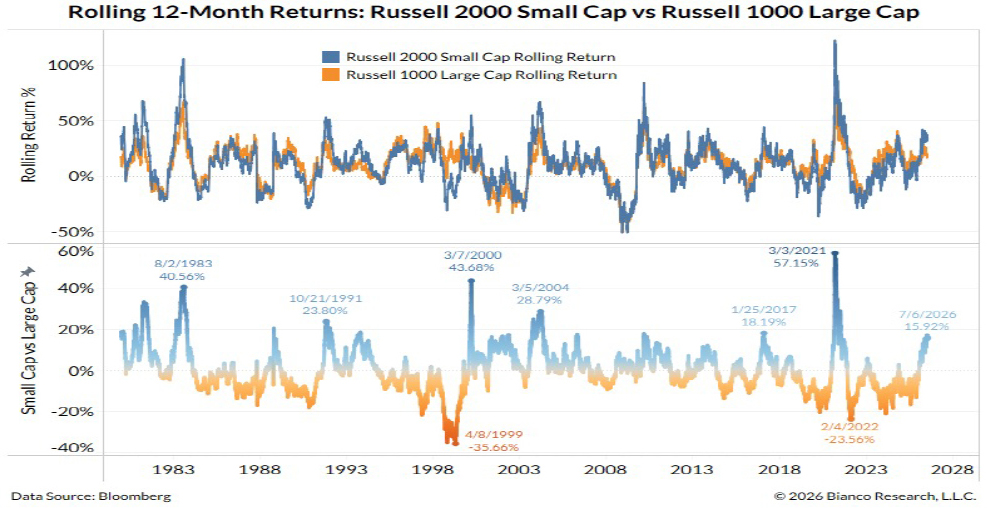

Equity leadership reversed from the first quarter. Technology and Industrials led as investors rewarded AI infrastructure, automation, data-center supply chains, and broader capital spending. Energy lagged as the oil spike faded. Small caps outperformed large caps, signaling that investors were beginning to price in a broader economic participation story tied to productivity gains and an AI spending cycle spreading across the broader economy.

The second-half setup is constructive, but more conditional than it appeared earlier in the year. The “two levers” framework of fiscal and monetary policy working together has, for now, narrowed into a single lever: fiscal policy. Tax relief, infrastructure investment, industrial incentives, deregulation, and AI-related capital spending remain meaningful supports for household cash flow, corporate investment, and productivity. Monetary policy, by contrast, is likely to remain on hold until the Committee gains confidence that the energy shock has fully exited headline inflation and that labor conditions have softened enough to justify easing.

That distinction matters. Fiscal policy can continue to support demand and capital formation, but it cannot fully offset the valuation and financing sensitivity of markets if the Fed remains patient. For now, the most likely path is no rate cuts and no rate hikes—a steady-but-watchful Fed. If oil’s quarter-end decline flows through headline inflation over the coming months, the door to lower rates could eventually reopen, particularly if labor markets show material deterioration.

The labor market remains best described as a low-hire, low-fire environment. Employers are not aggressively expanding headcount, but they are also not undertaking broad layoffs. That mix is consistent with slower growth rather than recession. It also gives the Fed optionality: a sudden weakening in claims, payrolls, or hours worked could quickly shift market expectations back toward rate cuts, while stable employment would allow Chairman Warsh to emphasize patience and data dependence.

Chairman Warsh enters at a difficult moment: one in which headline inflation has been distorted by energy shocks, core measures remain the true policy signal, and markets are highly sensitive to every change in tone. His early priority is likely to be reforming how the FOMC communicates uncertainty. Rather than presenting the Summary of Economic Projections as a point forecast, the Committee may place greater weight on scenario analysis, ranges, and the conditions that would trigger a change in policy. Warsh also appears focused on broadening the data set used to evaluate the economy—pairing traditional inflation and employment indicators with higher-frequency labor-market measures, inflation expectations, productivity data, and real-time indicators of household and business stress. The most important question is which inflation measure best captures underlying pressure after a temporary oil shock. In our view, the Fed will continue to look through volatile headline CPI when energy drives the move, leaning more heavily on core PCE, trimmed-mean measures, wage trends, and inflation expectations to determine whether policy is restrictive enough.

The U.S.–Iran MOU is a meaningful step toward de-escalation, but it is not yet a durable settlement. A credible, phased reopening of the Strait of Hormuz would help normalize shipping flows, reduce insurance and freight costs, and remove a significant geopolitical risk premium from oil markets. That would improve the inflation backdrop, support consumer purchasing power, and strengthen confidence in risk assets.

The principal risk is that the 60-day negotiation window functions as a pause rather than a bridge. A breakdown in talks, proxy escalation, slow implementation, or renewed threats to shipping lanes could quickly restore volatility in crude, freight, and inflation expectations. The investment conclusion is to stay constructive but not complacent: portfolios should participate in the relief rally while retaining exposure to quality, liquidity, and diversifying assets that can withstand another energy or geopolitical shock.

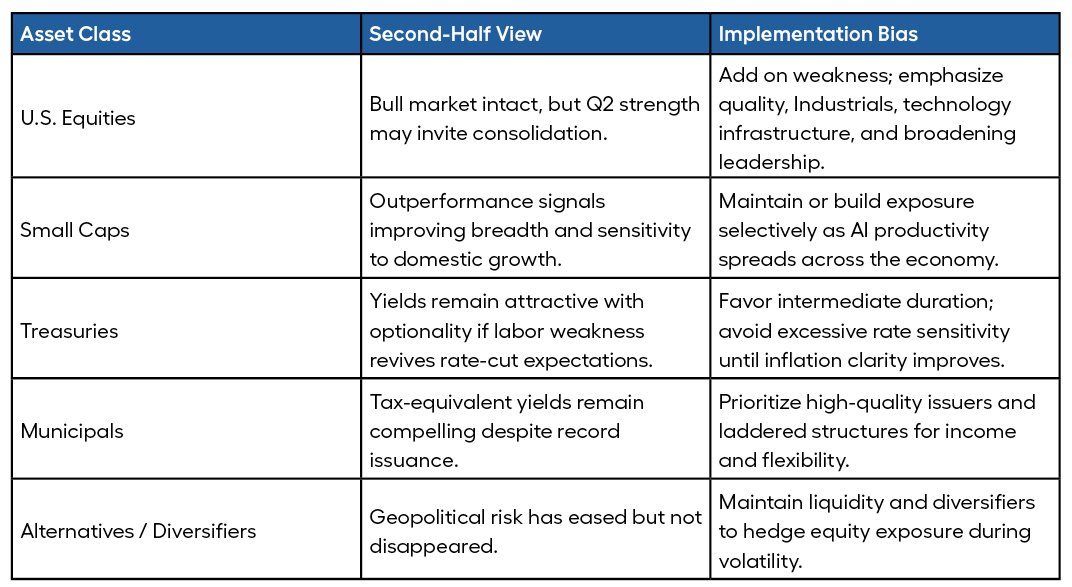

We continue to view the broader backdrop as consistent with an ongoing bull market. Economic activity remains resilient, earnings expectations are supported by productivity and margin discipline, and market breadth is improving. At the same time, the speed of the Q2 rally has left positioning more optimistic and valuations more dependent on execution. That does not end the bull market; it simply raises the probability of periodic pullbacks.

Potential sources of volatility include disappointment in the U.S.–Iran negotiation process, a renewed oil spike, a hotter-than-expected inflation print, uncertainty around Chairman Warsh’s communication framework, delayed rate-cut expectations, and excess enthusiasm around AI or new technology issuance. These are the types of interruptions that often occur within durable bull markets. Rather than trying to time the exact bottom, investors should use weakness to add exposure incrementally, emphasizing quality companies with durable earnings power, select cyclicals, and beneficiaries of productivity-enhancing capital spending.

The recent increase in technology IPOs, secondary offerings, and debt raises is another sign that capital markets are reopening and that investor risk appetite has improved. New issuance is often healthiest when it funds durable growth, and in today’s market much of the demand is tied to AI infrastructure, data centers, automation, and other productivity-enhancing investment themes. At the same time, rising supply can also be a signal that issuers are taking advantage of favorable windows and elevated valuations. For investors, the message is not to avoid the theme, but to be selective: favor companies with visible cash flows, credible profitability, and balance sheets capable of funding growth without relying entirely on optimistic capital-market conditions.

Small-cap leadership is an important development. If AI-driven productivity gains broaden across industries, the benefit should not remain confined to mega-cap platforms. Smaller domestic companies can gain from better demand, lower input volatility, automation, and improved operating leverage. A broader economy should produce broader stock-market participation, reinforcing the case for maintaining exposure beyond the largest technology names.

Fixed income remains attractive because yields are still competitive, even without immediate Fed cuts. Treasury yields continue to offer meaningful income and portfolio ballast, particularly in intermediate maturities where investors can capture carry while preserving flexibility if growth slows or the Fed eventually pivots. In a policy-on-hold environment, duration should be owned deliberately rather than aggressively: enough to hedge downside risk, but not so much that portfolios become overly exposed to renewed inflation volatility.

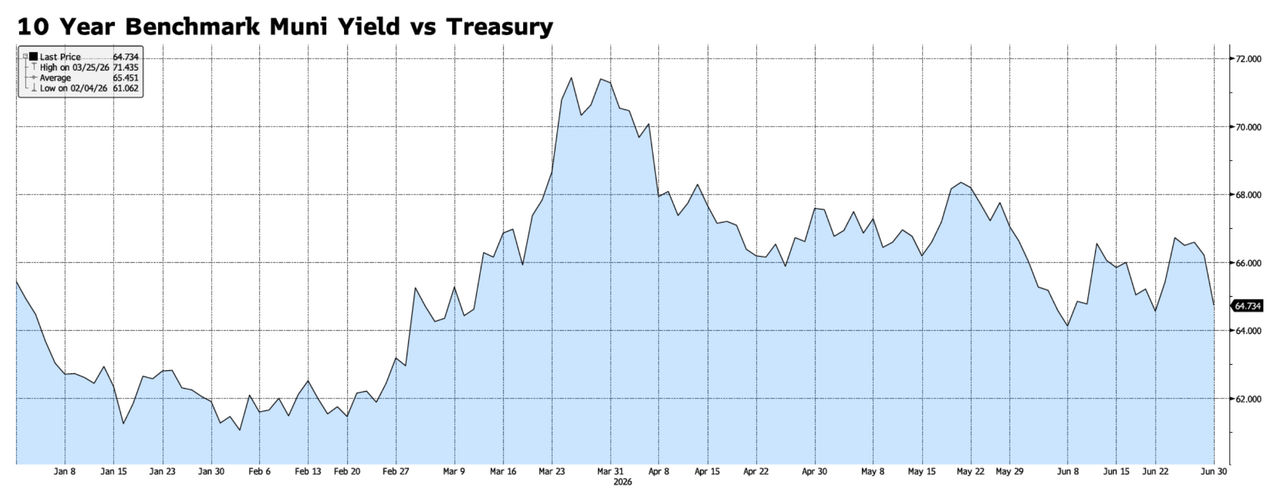

Municipal bonds remain especially compelling for tax-sensitive investors. Tax-equivalent yields are relatively attractive, credit quality remains broadly solid, and the market continues to absorb record issuance with significant inflows. That combination is notable: persistent demand despite heavy supply suggests investors continue to value after-tax income, diversification, and defensive characteristics. We would favor high-quality municipal exposure, with selectivity around issuer fundamentals, call structure, and curve positioning.

The upcoming mid-term elections will add another source of headline volatility, but divided government would not necessarily be a negative outcome for risk assets. Markets have often been comfortable with gridlock because it can reduce the probability of abrupt policy shifts, limit the scope for large new spending or tax changes, and force compromise around major legislation. That does not eliminate political risk; debt-ceiling negotiations, shutdown threats, regulatory priorities, and fiscal deadlines can still create periodic uncertainty. But from an investment perspective, gridlock can also provide a more stable policy backdrop, allowing earnings, rates, inflation, and productivity to remain the primary drivers of market performance. The key is to separate election-related noise from the underlying fundamentals: if growth remains resilient, inflation continues to ease, and corporate earnings hold up, a divided Washington could be more of a constraint on policy extremes than a reason to reduce exposure.

The second half of 2026 begins with a more constructive backdrop than appeared likely at the height of the Iran shock. Oil prices have retreated, the geopolitical risk premium has compressed, credit stress has remained contained, and equity leadership has broadened. The economy is not accelerating uniformly, but it continues to demonstrate resilience.

At the same time, the path forward is more dependent on fiscal support and productivity than on monetary easing. The Fed is likely to remain patient until the oil shock leaves headline inflation and labor-market data provide a clearer signal. That makes selectivity essential. We would remain positioned for growth, but with enough liquidity, quality, and income to use volatility deliberately.

In short, the investment message is constructive, not complacent. The fragile U.S.–Iran MOU can support a macro reset if it holds, AI-driven productivity can broaden market participation if it spreads, and fiscal policy can continue to lift growth even while monetary policy pauses. For clients, the discipline is straightforward: stay invested, diversify broadly, harvest income, and use market weakness as an opportunity to add to long-term themes.

Agentic AI continues to move from experimentation to enterprise adoption. The key investment opportunity is no longer limited to model builders; it increasingly includes infrastructure, automation, data management, cybersecurity, power demand, and companies using AI to expand margins.

Broader participation is a healthier foundation for the bull market. If productivity gains spread and financing conditions stabilize, small caps and cyclicals can benefit from operating leverage and improving domestic demand.

Tax-sensitive investors can use elevated municipal and Treasury yields to build durable income. Record muni issuance should be treated as an opportunity when paired with strong credit selection and laddered implementation.

The Strait of Hormuz shock has eased, but the 60-day window is fragile. Portfolios should preserve liquidity and diversification so volatility can be used as an entry point rather than becoming a forced-selling event.

Please reach out with any questions or to discuss portfolio positioning in more detail. We appreciate your continued trust and partnership.

If you are an existing customer and have Account related questions, please contact Customer Support.

Thank you for your feedback

Form submitted succesfully

By clicking submit, you understand the information is being provided to Flagstar Bank in accordance with our online privacy statement.

Important Legal Disclosures and Information

These materials are intended for distribution to Flagstar Private Bank clients, and do not constitute the provision of investment, legal, accounting, or tax advice to any person. This material presented is for informational purposes only and is not intended to be an offer, recommendation, or solicitation to purchase or sell any security or product, or to employ a specific investment or tax planning strategy. Forward looking projections are based on historical trends, actual results will differ. Past performance is no guarantee of future results.

The information contained herein was obtained from sources deemed reliable. Such information is not guaranteed as to its accuracy, timeliness, or completeness. The information contained and the opinions expressed herein are subject to change without notice, are those of the individual author(s), and may not necessarily represent the views of Flagstar Bank or any of its subsidiaries.

Flagstar Private Bank is a division of Flagstar Bank, N.A. (“Flagstar Bank”), Member FDIC. Flagstar Bank provides FDIC-insured banking products and services and lending of funds to individual clients. Securities, insurance, brokerage services, and investment advisory services are offered by Flagstar Securities, Inc. (“Flagstar Securities”), Member FINRA/SIPC, a registered broker-dealer and SEC registered investment adviser. Flagstar Securities is a wholly-owned subsidiary of Flagstar Bank.

Investments, Brokerage and Insurance Products Are:

Not Insured by the FDIC or Any Other Government Agency. | Not Bank Guaranteed. | Not Bank Deposits or Obligations. | May Lose Value.

|

Flagstar Securities Client Relationship Summary

Flagstar Securities Regulatory Summaries and Disclosures