INSIGHTS FROM THE PRIVATE BANK

THE POWER OF PERSPECTIVE

Brett Mitstifer, CFA

Flagstar Chief Investment Officer

FDIC-Insured—Backed by the full faith and credit of the U.S. Government

INSIGHTS FROM THE PRIVATE BANK

THE POWER OF PERSPECTIVE

Brett Mitstifer, CFA

Flagstar Chief Investment Officer

The third quarter of 2025 unfolded with a delicate balance between optimism and caution. Economic data suggested a 'Goldilocks' environment—growth was neither too hot nor too cold, with inflation steady at 2.6% and unemployment relatively steady at 4.3%. However, resilience was the true story, as markets absorbed shocks from tariff announcements, August’s soft retail sales, and September’s Fed rate cut. Payroll growth moderated, averaging 29,000 monthly additions, down from 171,000 in late 2024, indicating further evidence of a cooling labor market.

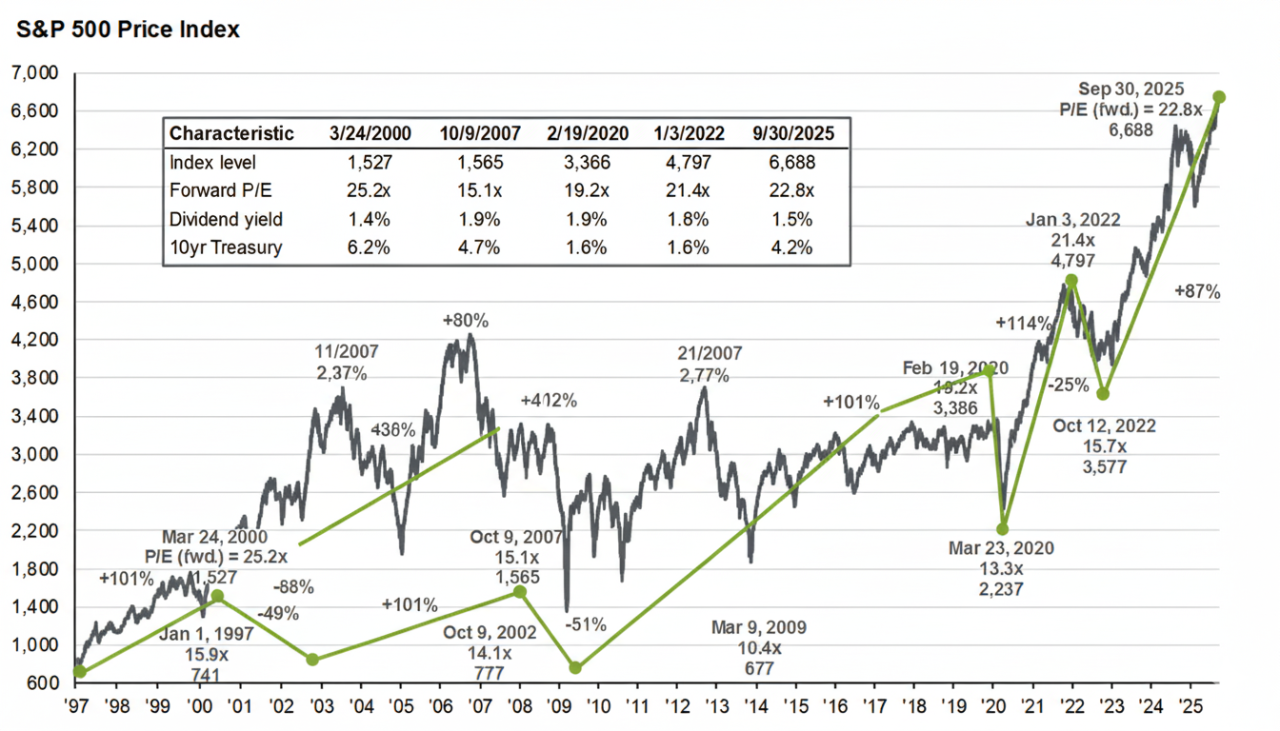

Despite these headwinds, the S&P 500 surged 7.8%, led by technology and communication services. Gains were driven by AI optimism and strong earnings, while energy lagged due to declining oil prices. International equities posted solid gains, with the MSCI ACWI ex-US rising 6.7% in USD terms. However, U.S. equities outpaced global peers, driven by strong earnings and dollar stabilization. Approximately 81% of S&P 500 companies beat EPS estimates, reflecting corporate resilience despite tariff uncertainty.

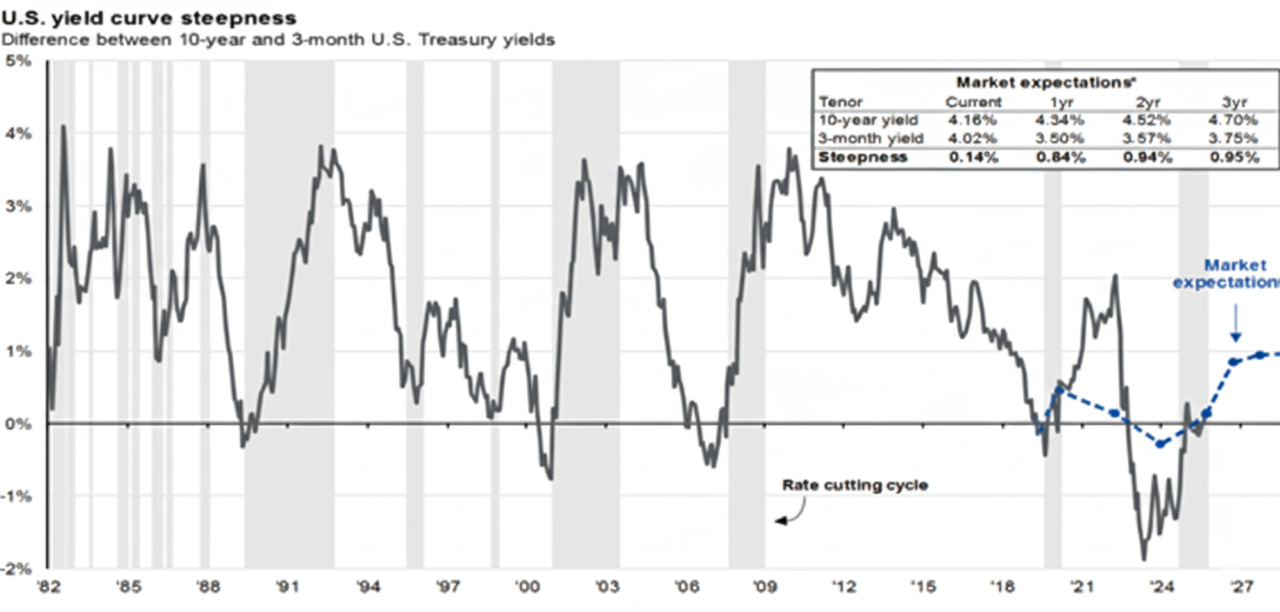

Fixed income markets were mixed. Treasury yields fluctuated between 4.0% and 4.5%, balancing fiscal concerns with slowing growth. High-yield bonds gained 2.5%, while municipal bonds lagged slightly amid supply pressures and investor rotation toward higher-yielding credit. The Fed’s September rate cut marked its first in 2025, citing labor market softness and elevated inflation. Policymakers projected two additional cuts by year-end.

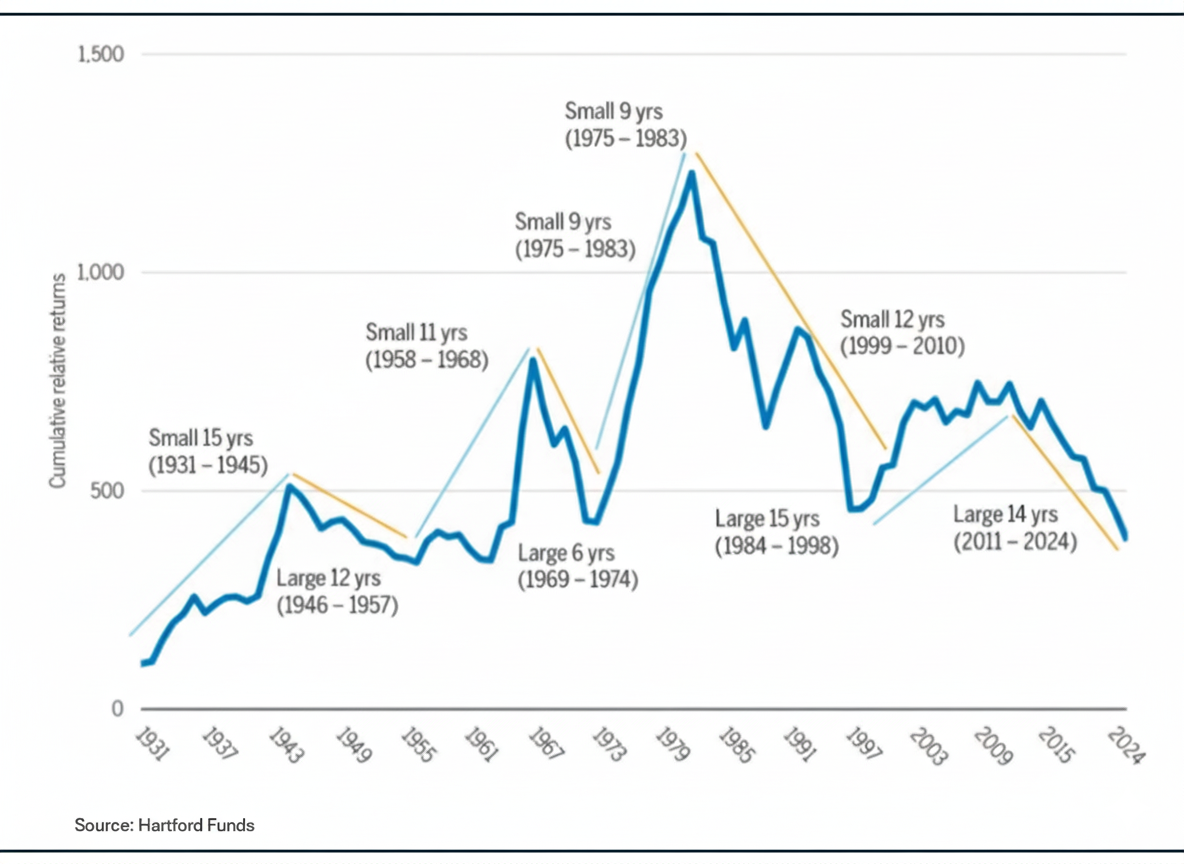

Looking forward from the end of Q3 into Q4 and 2026, signs of market broadening beyond the Magnificent 71 are emerging. While mega-cap tech names have dominated performance, recent dispersion in returns and volatility suggests a shift in leadership. Capital is increasingly flowing into small- and mid-cap equities, value-oriented sectors, and international markets, creating a more diversified opportunity set.

Lower interest rates provide a supportive backdrop for equities. With inflation contained and the Fed expected to continue easing, equity valuations—particularly outside of large-cap growth—appear increasingly attractive. The anticipated decline in the fed funds rate to around 3.0% by 2026 should help sustain earnings growth and improve financing conditions.

Corporate earnings remain a key driver of equity performance. Despite tariff-related uncertainty, Q2 earnings beat expectations, and consensus forecasts point to continued growth into 2026. Sectors tied to infrastructure, defense, and AI innovation are particularly well-positioned. We expect earnings growth to accelerate as trade tensions ease and fiscal stimulus supports demand. Looking forward from the end of Q3 into Q4 and 2026, signs of market broadening beyond the Magnificent 7 are emerging. While mega-cap tech names have dominated performance, recent dispersion in returns and volatility suggests a shift in leadership. Capital is increasingly flowing into small- and mid-cap equities, value-oriented sectors, and international markets, creating a more diversified opportunity set.

The Fed’s September cut steepened the short end of the curve, while longer-term yields remained steady. Credit spreads remain tight, especially in BBB-rated bonds, suggesting low recession risk. Municipal bonds offer attractive after-tax yields, particularly in the intermediate part of the curve. Despite modest underperformance in Q3, technicals are expected to improve, and supply-demand dynamics remain favorable for tax-exempt investors. We maintain a neutral stance between Treasuries and credit, recognizing relative value in both sectors depending on duration and risk appetite. Resilience in corporate fundamentals supports a balanced approach across duration and credit quality.

We remain vigilant and flexible in our positioning, ready to adjust portfolios as conditions evolve. Diversification, quality, and active management will be key to navigating the year ahead.

The third quarter of 2025 showcased a market environment that many might label “Goldilocks”—not too hot, not too cold. Inflation moderated, growth remained steady, and the Fed began easing rates. But beneath the surface, it was resilience that truly defined the quarter. Markets absorbed tariff shocks, policy uncertainty, and mixed economic data, yet still delivered strong performance across equities and credit.

Understanding the difference is more than semantics. The Goldilocks economy implies a stable, low-volatility environment where investors can rely on consistent growth and policy support. Resilience, on the other hand, reflects an economy and market that can withstand shocks, adapt to change, and recover quickly—even if the path is uneven.

As we look ahead to 2026, this distinction will shape investment strategy. If conditions remain Goldilocks-like, risk assets may continue to benefit from low rates and steady earnings. But if resilience is the dominant theme, investors will need to prioritize flexibility, quality, and diversification to navigate volatility and seize opportunities in a more dynamic landscape. Lower interest rates, broadening equity leadership beyond mega-cap tech, and improving earnings visibility all support a positive outlook. In fixed income, tight credit spreads and attractive tax-exempt yields offer compelling relative value, though selectivity remains key.

We remain focused on positioning portfolios to thrive in either scenario—balancing growth potential with downside protection, and staying agile as the macro environment evolves.

Please reach out with any questions or to discuss portfolio positioning in more detail. We appreciate your continued trust and partnership.

If you are an existing customer and have Account related questions, please contact Customer Support.

Thank you for your feedback

Form submitted succesfully

By clicking submit, you understand the information is being provided to Flagstar Bank in accordance with our online privacy statement.

Important Legal Disclosures and Information

These materials are intended for distribution to Flagstar Private Bank clients, and do not constitute the provision of investment, legal, accounting, or tax advice to any person. This material presented is for informational purposes only and is not intended to be an offer, recommendation, or solicitation to purchase or sell any security or product, or to employ a specific investment or tax planning strategy. Forward looking projections are based on historical trends, actual results will differ. Past performance is no guarantee of future results.

The information contained herein was obtained from sources deemed reliable. Such information is not guaranteed as to its accuracy, timeliness, or completeness. The information contained and the opinions expressed herein are subject to change without notice, are those of the individual author(s), and may not necessarily represent the views of Flagstar Bank or any of its subsidiaries.

Flagstar Private Bank is a division of Flagstar Bank, N.A. (“Flagstar Bank”), Member FDIC. Flagstar Bank provides FDIC-insured banking products and services and lending of funds to individual clients. Securities, insurance, brokerage services, and investment advisory services are offered by Flagstar Securities, Inc. (“Flagstar Securities”), Member FINRA/SIPC, a registered broker-dealer and SEC registered investment adviser. Flagstar Securities is a wholly-owned subsidiary of Flagstar Bank.

Investments, Brokerage and Insurance Products Are:

Not Insured by the FDIC or Any Other Government Agency. | Not Bank Guaranteed. | Not Bank Deposits or Obligations. | May Lose Value.

|

Flagstar Securities Client Relationship Summary

Flagstar Securities Regulatory Summaries and Disclosures

For Educational Purposes Only.

Implied or Referenced Data Sources:

- U.S. Bureau of Labor Statistics (BLS); Unemployment rates, non-farm payroll data, and labor market trends.

- Federal Reserve (FOMC Statements & Economic Projections); Interest rate decisions, rate cut announcements, and policy outlook.

- U.S. Department of Commerce / Bureau of Economic Analysis (BEA); Inflation metrics such as Core PCE (Personal Consumption Expenditures).

- S&P Global / FactSet / Bloomberg; S&P 500 performance, earnings beat statistics, sector performance, and equity market data.

- MSCI Inc.; MSCI ACWI ex-US index performance.

- Jackson Hole Symposium (Federal Reserve Bank of Kansas City); Themes and discussions around labor market transitions and productivity.

- World Economic Forum – Chief Economists’ Outlook; Global economic uncertainty and AI-driven disruption.

- Company Earnings Reports (e.g., Nvidia); Specific corporate performance and earnings surprises.

- Market Data Providers (e.g., ICE, LSEG, Morningstar); Treasury yields, municipal bond performance, and credit spreads.

- Geopolitical News Sources (e.g., Reuters, Bloomberg, Financial Times); Trade agreements, geopolitical tensions, and oil price movements.